Chargeback insurance helps businesses recover losses from fraud-related chargebacks, such as those caused by stolen credit cards or fraudulent transactions. While it can protect merchants from significant financial hits, it comes with limitations, high costs, and specific eligibility requirements. Here’s what you need to know:

Key Takeaways:

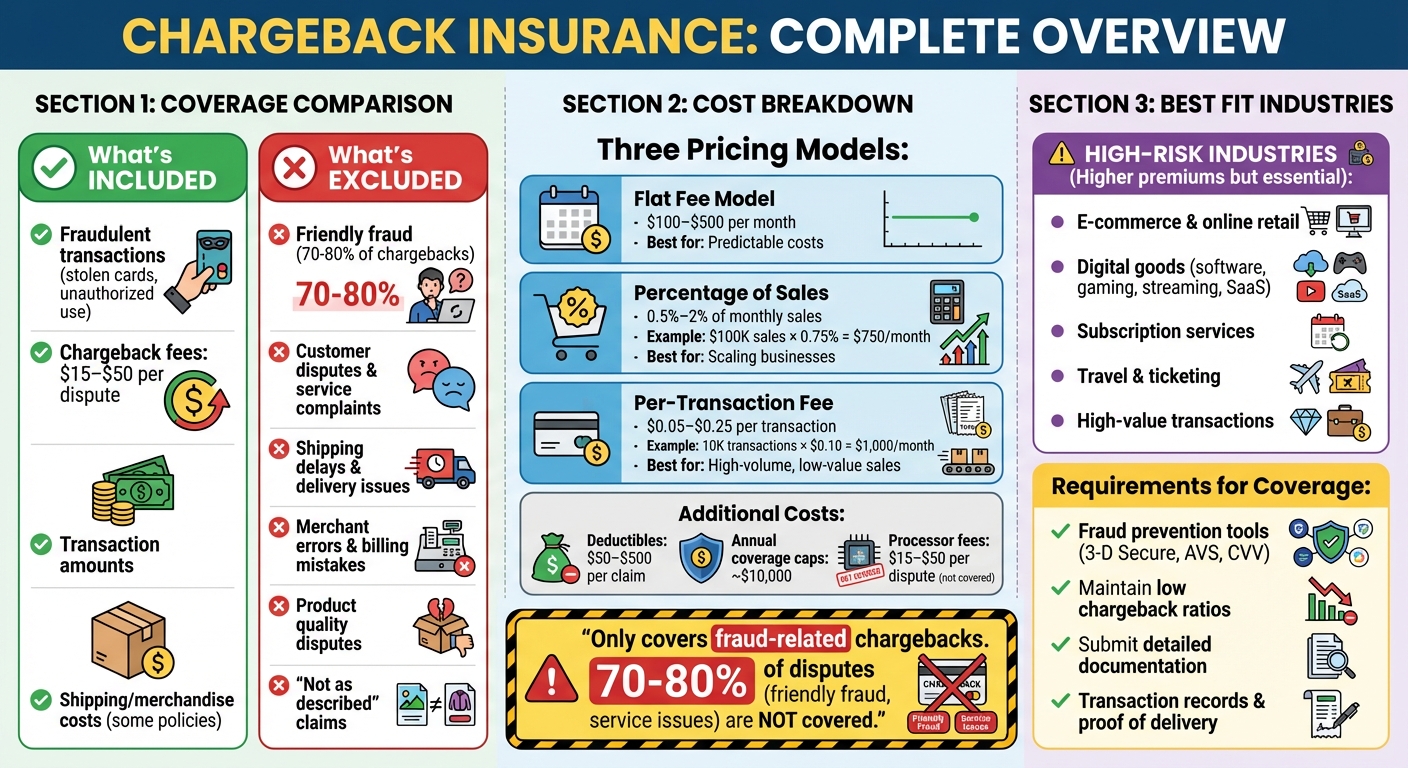

- What It Covers: Fraudulent transactions, chargeback fees ($15–$50), and sometimes shipping or merchandise costs.

- What It Doesn’t Cover: Friendly fraud, service disputes, shipping issues, or merchant errors.

- Costs: Premiums vary by risk level and pricing model – flat fees ($100–$500/month), percentages of sales (0.5%–2%), or per-transaction fees ($0.05–$0.25).

- Requirements: Merchants must use fraud prevention tools like AVS, CVV checks, or 3-D Secure and maintain low chargeback ratios.

- Who Benefits Most: High-risk industries like e-commerce, digital goods, travel, and subscription services.

Quick Comparison:

| Aspect | Included | Excluded |

|---|---|---|

| Covered Chargebacks | Fraudulent transactions | Friendly fraud, customer disputes |

| Costs Reimbursed | Transaction amount, fees | Merchant errors, quality issues |

| Premiums | $100–$500/month or 0.5%–2% sales | Deductibles reduce payouts |

| Best Fit Businesses | High-risk industries, e-commerce | Low-risk businesses, few disputes |

Chargeback insurance works best as part of a broader strategy that includes fraud prevention tools and dispute management. Assess your chargeback data and evaluate if insurance costs outweigh potential benefits. For many, improving internal processes and working with payment providers like Secured Payments may offer better value.

Chargeback Insurance Coverage, Costs, and Pricing Models Comparison

What You Need to Know About Chargeback Insurance

Chargeback insurance helps businesses recover losses from fraud-related chargebacks, like those caused by stolen credit cards or unauthorized account use. It typically covers the disputed transaction amount, chargeback fees (which often range from $15 to $50), and in some cases, costs for shipping or merchandise. For example, if a fraudulent $500 purchase occurs, the policy can reimburse both the transaction amount and associated fees, provided the necessary documentation is submitted.

However, this type of insurance is mainly focused on fraud-based disputes. It doesn’t cover issues like customer dissatisfaction, service complaints, shipping delays, or errors made by the merchant. Additionally, policies often exclude transactions that surpass certain limits, occur in restricted regions, or involve high-risk products.

For online merchants and businesses operating in high-risk industries, chargeback insurance can be especially helpful. E-commerce sellers, particularly those offering digital goods like software, gaming content, streaming services, or SaaS, often find this coverage essential since proving delivery can be tricky. It’s also valuable for businesses with high-value transactions, slim profit margins, or smaller operations that lack dedicated fraud management teams.

To qualify for a policy, merchants are usually required to implement fraud prevention tools such as 3-D Secure, Address Verification System (AVS), or CVV checks. When a covered chargeback occurs, the merchant submits transaction records and proof of delivery to the insurer, who then reimburses losses up to the policy’s limits after deductibles. Many insurers also require merchants to maintain specific chargeback ratios and use approved fraud prevention measures – failing to meet these conditions can void the policy.

The cost of chargeback insurance depends on factors like industry risk, a merchant’s chargeback history, transaction size, and sales volume. Pricing models vary and might include a percentage of transactions, a per-dispute fee, or a flat premium with deductibles. Businesses in higher-risk sectors, such as digital goods, travel, and subscription services, often face steeper premiums. However, choosing a higher deductible can reduce premiums by transferring more of the initial loss to the merchant.

1. Protection from Large Fraud Losses

Coverage Scope and Limitations

Chargeback insurance steps in when your business faces significant losses due to fraudulent transactions. Imagine this: a stolen credit card is used to make a $5,000 purchase from your online store. When the cardholder disputes the charge, this insurance can help cover the transaction amount, the product cost, and any related fees. It’s specifically designed to handle issues like unauthorized transactions, criminal fraud, or technical errors that lead to disputes.

That said, the coverage is limited to actual fraud cases. If a dispute arises from customer dissatisfaction, buyer’s remorse, or service complaints – commonly referred to as "friendly fraud" – those scenarios aren’t covered. This targeted approach ensures the insurance focuses on protecting you from the most damaging types of fraud.

Risk Mitigation Benefits

The financial burden of fraudulent chargebacks can be overwhelming, especially for small businesses. A single fraudulent chargeback often costs more than double the original transaction amount due to dispute and chargeback fees. For a small business operating on tight margins, recovering from a $10,000 fraudulent chargeback without insurance could spell disaster. Chargeback insurance helps absorb these unexpected costs, providing a safety net that could make the difference between staying in business and shutting down.

Integration with Broader Fraud Prevention Strategies

Chargeback insurance works best when paired with proactive fraud prevention efforts. Many providers enhance their insurance offerings with tools like real-time alerts and transaction monitoring to catch suspicious activity before it escalates. For instance, payment partners like Secured Payments offer high-risk merchant accounts and e-commerce processing solutions equipped with built-in fraud detection. Combining insurance with these tools not only lowers costs but also reinforces your overall approach to managing risk effectively.

2. Reimbursement of Fees and Related Expenses

Coverage Scope and Limitations

Chargeback insurance helps cover fees charged by your acquiring bank, which typically range from $15 to $50 per dispute. In more complex cases, these fees can be even higher. Beyond these charges, policies often reimburse wholesale costs and lost profit margins. Some policies may even cover certain legal expenses tied directly to chargeback disputes, though these types of reimbursements are less common and usually come with limits. This feature adds an extra layer of financial protection for merchants.

However, reimbursement is limited to fraudulent or unauthorized transactions. Issues like friendly fraud, customer complaints about service, delivery problems, or disputes over items not matching descriptions are excluded from coverage. Additionally, failing to follow required fraud prevention measures – such as Address Verification Service (AVS) or Card Verification Value (CVV) checks – or neglecting to submit proper documentation can lead to claim denials.

Risk Mitigation Benefits

Chargebacks can cost merchants significantly more than the original transaction amount when fees and other overhead are factored in. For example, if an e-commerce apparel store loses $200 in revenue and incurs a $25 fee, the financial hit adds up quickly. Without coverage, this loss can be substantial. Chargeback insurance can help recover these costs, including part of the lost profit.

Integration with Broader Fraud Prevention Strategies

To ensure reimbursement claims are valid, merchants often need to integrate their payment systems with advanced fraud prevention tools provided by their insurance provider. These tools enable real-time transaction scoring and approvals. Claims must also be submitted promptly with all required documentation, such as order details, proof of delivery, and communication records, to avoid rejection.

Providers like Secured Payments offer integrated solutions, combining chargeback insurance with high-risk merchant account services. These systems work together to fine-tune fraud filters and pre-authorization checks, ensuring merchants maintain eligibility for reimbursement while minimizing fraud risks.

3. Limited Coverage and Exclusions

Coverage Scope and Limitations

When it comes to chargeback insurance, understanding its limits is key to managing risk effectively. This type of insurance typically covers only fraudulent transactions, such as card-not-present fraud or stolen card use. However, this leaves a significant gap, as 70–80% of chargebacks – like those stemming from other disputes – aren’t covered.

For instance, friendly fraud, where customers dispute charges despite receiving their orders, is excluded. Other exclusions include complaints about product quality, billing errors by the merchant, duplicate charges, or claims that items were "not as described." Imagine an online retailer facing a $500 chargeback over a product quality issue – this wouldn’t be covered under such policies.

Coverage also comes with limits and deductibles. Policies often cap annual reimbursements at around $10,000, and deductibles can range from $50 to $500 per claim, reducing the amount merchants can recover. For example, if a fraudulent chargeback is $200 and the deductible is $100, the merchant would only recover $100. Additionally, businesses in high-risk industries may face extra fees of $15 to $50 per dispute.

The claims process is another hurdle. Insurers typically require detailed documentation, such as transaction records, signed delivery receipts, tracking numbers, and IP logs. Missing even one key piece of evidence – like a shipping confirmation for a $300 dispute – can result in a denied claim, leaving the merchant to absorb the loss and associated fees. This highlights the importance of using fraud detection tools from providers like Secured Payments to strengthen evidence and reduce risk.

Certain industries face even tighter restrictions. Sellers of digital goods, online gaming platforms, CBD products, and subscription services often encounter exclusions or reduced coverage due to their higher fraud risks. For example, disputes over the quality of a digital service might not be covered at all, leaving these businesses particularly vulnerable.

sbb-itb-8c45743

4. High Premiums and Deductibles

Cost and Pricing Models

Chargeback insurance often comes with steep costs, making it a tough choice for small businesses or those with tight profit margins. Insurers typically use one of three pricing structures: a flat monthly or annual fee, a percentage of sales (commonly 0.5%–1% of gross processing volume for high-risk merchants), or a per-transaction fee. Businesses in high-risk industries – like subscription services, digital goods, or travel – pay even higher rates because insurers anticipate more frequent and larger claims.

On top of premiums, merchants face deductibles ranging from $50 to $500 per incident, along with potential aggregate deductibles. This means the coverage is better suited for shielding against major fraud losses rather than smaller, everyday disputes. These costs force businesses to carefully balance the immediate expense of insurance against the potential savings from reduced fraud losses.

When High Costs Outweigh Benefits

For many merchants, the math doesn’t always work out in their favor. Take, for example, a U.S.-based online business processing $2,000,000 annually with $40,000 in chargeback losses – only $20,000 of which is clearly tied to criminal fraud. If the merchant pays a 0.6% premium ($12,000 per year), has a $50 deductible, and deals with 150 qualifying disputes averaging $150 each, the gross reimbursable amount would total $22,500. However, after deducting $7,500 in deductibles (150 × $50), the net reimbursement drops to $15,000. In this scenario, the merchant ends up with just a $3,000 gain after paying premiums – and still has to cover chargebacks that aren’t insured.

Beyond these direct costs, merchants also face additional fees from acquirers, which typically range from $15 to $50 per dispute, as well as the operational burden of filing claims. If most disputes are related to issues like "item not as described" or service-related complaints – categories often excluded from coverage – the insurance might offer little practical benefit.

Integration with Broader Fraud Prevention Strategies

Instead of relying solely on chargeback insurance, many merchants find better value by investing in fraud prevention tools and working with payment providers that specialize in risk management. Companies like Secured Payments offer services such as integrated e-commerce payment processing, support for high-risk merchant accounts, and tailored consulting to strengthen fraud defenses. These solutions reduce chargeback rates by implementing advanced authorization rules, real-time fraud screening, and efficient dispute handling – minimizing the need for expensive insurance premiums.

5. How Payment Partners like Secured Payments Help

Risk Mitigation Benefits

Payment partners tackle chargeback issues right at their source. Take Secured Payments, for instance – they use real-time fraud screening, AVS/CVV checks, and velocity rules to block suspicious transactions before they’re even authorized. This proactive approach addresses problems that chargeback insurance often doesn’t cover, like unclear billing descriptors, shipping delays, or weak refund policies. These issues can lead to friendly fraud or service disputes if left unchecked.

For U.S. merchants, especially those operating in high-risk areas like digital goods or subscription services, this first line of defense is invaluable. A skilled payment partner is familiar with U.S. card network patterns and common fraud tactics – like card-not-present attacks in e-commerce – and can adjust authorization rules to stay ahead of evolving threats. The payoff? Fewer disputes overall, which means lower penalties from processors, better merchant account terms, and reduced overall risk. This kind of proactive fraud prevention is a cornerstone of a solid risk management strategy.

Integration with Broader Fraud Prevention Strategies

Beyond these initial safeguards, payment partners play a key role in streamlining risk management across the board. A strong payment partner oversees the entire transaction process – from authorization to post-sale support. Secured Payments, for example, provides an all-in-one solution that combines fraud detection tools, chargeback alerts, automated evidence collection, and dispute management. This integrated approach ensures disputes are either prevented, effectively challenged with solid evidence, or reimbursed according to clear guidelines.

The numbers speak for themselves: professional chargeback management can win 60–80% of representments, compared to the limited scope of insurance that only covers some fraud-related disputes. Payment partners gather critical evidence, such as device data, IP addresses, delivery confirmations, and usage logs, to help merchants overturn friendly fraud claims. This is especially crucial for businesses with tight margins or rapid growth, where just a few large fraudulent transactions could severely disrupt cash flow. With strong pre-transaction controls and effective post-transaction dispute handling, merchants are better equipped to protect their bottom line.

Pricing Models and Cost Breakdown for Chargeback Insurance

Understanding pricing models is essential when evaluating chargeback insurance options. Providers generally offer three main pricing structures: a flat monthly or annual fee, a percentage of sales volume, or a per-transaction charge. Each structure affects costs differently, depending on your business size and risk profile. Let’s break these down.

Flat-fee policies involve a fixed monthly or annual payment, typically ranging from $100 to $500 per month for high-risk e-commerce businesses. This model provides consistent, predictable costs, which can appeal to U.S. merchants with steady sales volumes. However, if your business experiences few chargebacks, you might end up paying more in premiums than you save in fraud-related losses.

The percentage-of-sales model adjusts based on your monthly revenue. Policies often charge between 0.5% and 2% of sales, with some offering lower rates (0.4%–0.9%) for card-not-present transactions. For instance, a business processing $100,000 in monthly sales at a 0.75% rate would pay $750. While this model scales with your growth, high-volume merchants may find costs increasing significantly even if their fraud risk remains low.

Per-transaction fees apply a small charge to each sale, typically $0.05–$0.25 or 0.1%–0.5% of the transaction value. For example, a business with 10,000 transactions a month at $0.10 per transaction would pay $1,000. This model is often a better fit for businesses with lower average order values, such as subscription services, since it avoids large upfront commitments.

To choose the right model, calculate your annual chargeback losses, factoring in both transaction values and additional processor fees (usually $20–$100 per dispute). Compare these losses to the total premiums for each pricing structure. Keep in mind that most policies only cover criminal fraud chargebacks, not disputes caused by friendly fraud or merchant errors. If your fraud-related losses regularly exceed 0.5% of sales, chargeback insurance could be a cost-effective solution.

When to Use Chargeback Insurance and How to Combine It with Risk Management

Before purchasing chargeback insurance, take a moment to assess your fraud-driven chargeback rate – this is the percentage of transactions flagged as "unauthorized" or "does not recognize." If your rate is consistently hovering around 0.9–1.0% or higher, and the majority of disputes are tied to stolen cards rather than service-related complaints, insurance might be a worthwhile investment. Industries like U.S. e-commerce, subscription services, digital goods, travel, and ticketing are particularly vulnerable to criminal fraud, making them prime candidates for this type of protection. This evaluation lays the groundwork for integrating insurance with a broader risk management plan.

Skip insurance if most of your disputes arise from friendly fraud, shipping problems, or product complaints. These policies typically cover only clearly fraudulent, unauthorized transactions – not cases where customers claim "item not received" or "not as described." In such scenarios, your resources are better spent improving customer service, refining billing descriptors, or tightening your shipping and fulfillment processes. Businesses with chargeback rates well below the thresholds set by payment networks and strong fraud controls in place often find little value in paying insurance premiums.

Layered protection is key to minimizing risk. Use tools like real-time fraud scoring and device fingerprinting to block fraudulent activity before it even reaches your payment gateway. For high-risk or high-value transactions, implement 3-D Secure authentication to shift liability away from your business. Chargeback alerts can also help you intercept disputes early, giving you a chance to resolve them before they officially hit your account. Insurance should be reserved as a final safety net, covering the fraud that manages to slip through your other defenses.

To bring all these measures together, partnering with payment experts can offer a strategic advantage. Companies like Secured Payments can analyze your transaction history, dispute ratios, and overall risk profile to determine whether insurance is a good fit for your business. They can help you integrate fraud prevention tools, chargeback monitoring, and dispute management into a single, streamlined strategy. This ensures you’re not spending money on overlapping protections. For merchants in high-risk industries or those experiencing rapid growth, such expertise can help you strike the right balance between prevention, operational improvements, and financial coverage.

Revisit your strategy every 3–6 months. Compare your insurance premiums to the reimbursements you’ve received, monitor changes in your chargeback rate, and review any claims denied due to policy exclusions. If your fraud prevention tools improve or your risk profile shifts – such as entering new markets or implementing stricter processes – you may be able to scale back coverage to focus only on the most vulnerable transactions or even phase out insurance altogether in favor of stronger internal controls.

Conclusion

Chargeback insurance offers U.S. businesses a safety net against substantial losses from fraudulent chargebacks, helping to stabilize cash flow. This can be especially useful for industries like e-commerce, digital goods, travel, and subscription services. However, it’s important to note that the coverage is limited – it doesn’t extend to issues like friendly fraud, shipping problems, or service-related disputes. If your disputes primarily fall outside the covered categories, the high premiums and uncovered losses could outweigh the benefits.

To determine whether chargeback insurance is right for your business, start by analyzing 6–12 months of chargeback data. Break it down by cause, and calculate your total losses, including fees and labor. Compare this to the projected cost of premiums. If most of your disputes stem from non-fraud-related issues or your chargeback rate is already low, you might find better value in investing in fraud prevention tools, improving billing clarity, enhancing customer service, or streamlining operations.

For a more tailored approach, consider working with experts like Secured Payments. They can help you analyze your transaction history, identify dispute trends, and assess your overall risk profile. Their comprehensive solutions focus on fraud prevention, transaction routing, and dispute management, ensuring you avoid unnecessary costs and reliance on a single tool.

Ultimately, chargeback insurance works best as a backup plan within a broader risk management strategy. As your business grows and evolves – whether through changes in sales volume, product offerings, or fraud trends – regularly reassess the role of insurance. Prioritize proactive measures to reduce chargebacks before they happen, ensuring your approach remains effective and cost-efficient.

FAQs

What should businesses consider before getting chargeback insurance?

When looking into chargeback insurance, businesses need to consider a few key factors. Start with your transaction volume, risk level, and industry type, as these directly influence both the cost and scope of coverage. It’s equally important to evaluate the insurer’s track record, the policy’s coverage limits, and any exclusions to make sure it fits your payment processing requirements.

Another critical aspect is how the insurance could affect your cash flow. Weigh the costs versus the potential benefits to determine if it’s a worthwhile investment. By taking the time to dig into these details, you’ll be better equipped to choose a policy that provides the right level of protection for your business.

How can businesses combine chargeback insurance with their fraud prevention efforts?

To get the most out of chargeback insurance while tackling fraud, businesses should adopt a multi-layered strategy. This means combining proactive security tools with financial safeguards. For instance, tools like real-time transaction monitoring, Address Verification Service (AVS), and CVV verification can help identify and block fraudulent activities before they escalate into chargebacks.

When you pair chargeback insurance with these fraud prevention measures, you’re not only minimizing the financial blow from fraud but also ensuring coverage for those chargebacks that are unavoidable. Strengthen this approach by keeping your fraud detection systems up to date and training your team to recognize red flags. Together, these efforts create a solid shield against chargeback-related risks.

What exclusions should businesses know about when it comes to chargeback insurance?

Businesses should be aware that chargeback insurance policies often come with exclusions. Some of the most common exclusions include disputes linked to fraud, claims involving intentional wrongdoing, problems arising from customer dissatisfaction with a product or service, and transactions related to high-risk industries or restricted items.

It’s crucial to have a clear understanding of these exclusions to ensure your business is properly safeguarded and to prevent unexpected outcomes when submitting a claim.