Central Bank Digital Currencies (CBDCs) are reshaping how central banks manage monetary policy. These digital currencies, issued directly by central banks, can improve how policy rates impact households and businesses. However, they also pose risks to financial stability, especially for banks. Here’s what you need to know:

-

What are CBDCs? Digital currencies issued by central banks, divided into two types:

- Retail CBDCs: For everyday use by individuals and businesses.

- Wholesale CBDCs: For financial institutions and large transactions.

- Why they matter: CBDCs can make monetary policy more efficient by directly influencing deposit and loan rates, bypassing traditional intermediaries like banks.

- Key risks: They could disrupt bank funding, increase loan costs, and heighten risks of digital bank runs during crises.

- Potential solutions: Design choices like interest rate caps, holding limits, and safeguards to prevent rapid deposit outflows.

CBDCs could modernize monetary systems, but their success depends on balancing benefits with risks to ensure financial stability.

How CBDCs Change Monetary Policy Tools

CBDC Impact on Bank Deposit Rates and Profit Margins

Interest-Bearing CBDCs as Policy Instruments

An interest-bearing CBDC could add a new dimension to the Federal Reserve’s toolkit, providing a direct policy rate that impacts households and businesses without relying on commercial banks as intermediaries. Currently, the Fed influences short-term rates through mechanisms like the federal funds rate and interest on reserves. But with an interest-bearing CBDC, it could establish a direct rate for digital dollars.

If broadly accessible, this CBDC rate would act as a universal floor for deposit and short-term market rates. The reasoning is simple: no rational saver would settle for a lower return from a bank when they could earn more on a risk-free CBDC with similar safety. By setting the CBDC rate at either 0% or slightly below the policy rate – say, 1 percentage point lower – the Fed could enhance monetary transmission while managing the risk of excessive deposit outflows.

CBDCs might also solve the zero lower bound issue that has limited the Fed’s flexibility during severe downturns. Pairing an interest-bearing CBDC with restrictions on paper cash could allow the central bank to implement deeply negative interest rates if necessary, reducing reliance on unconventional tools like quantitative easing. This could make monetary policy more effective in influencing borrowing costs for consumers and businesses, though it would require clear communication and public acceptance of potentially negative rates on retail accounts.

Effects on Money Supply and Bank Lending

The introduction of CBDCs would reshape traditional funding channels, significantly impacting bank lending and financial stability. When households and businesses move funds into CBDC accounts, banks lose deposits, which are their primary funding source. To compensate, banks might turn to costlier alternatives like wholesale funding, long-term debt, or even borrowing from the central bank to sustain their lending activities.

While banks can adapt to these changes, constraints such as collateral shortages and liquidity pressures could amplify the impact on credit availability. This might result in higher loan rates or reduced loan volumes, particularly for smaller or riskier borrowers. The extent of this disruption would depend on how the CBDC is designed – factors like its interest rate, holding limits, and access rules would play a major role – as well as the availability of other safe assets like Treasury bills and money market funds.

The interest rate channel of monetary policy could strengthen with CBDCs, as a risk-free, transparent CBDC rate would more closely align policy rates with deposit and loan rates. However, the bank lending channel might become more sensitive to economic conditions. In stable periods, the Federal Reserve could offset funding changes, but during times of stress, liquidity or capital constraints could magnify CBDC-induced shifts, potentially limiting banks’ ability to extend credit. These changes would directly affect bank competition and the overall efficiency of monetary policy.

Economic Impact of CBDC Adoption

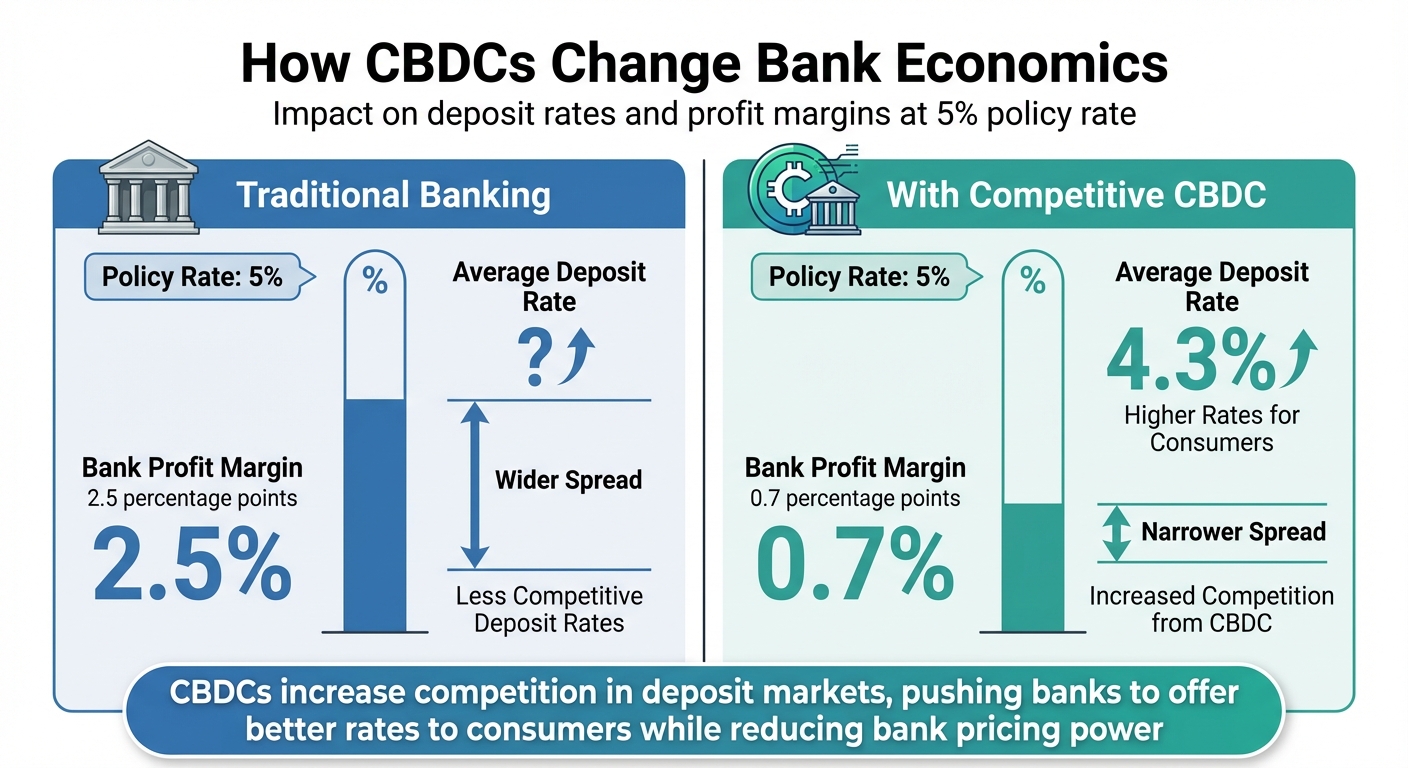

A well-designed CBDC could increase competition in deposit markets, pushing banks to offer better rates. For example, with a policy rate of 5%, the average deposit rate could rise to 4.3%, narrowing the spread to just 0.7 percentage points. This would reduce banks’ pricing power and improve the speed and effectiveness of monetary policy transmission.

Research and simulations suggest that a thoughtfully implemented CBDC could enhance economic welfare by improving monetary policy efficiency, reducing frictions in deposit markets, and expanding financial access. Studies also indicate that CBDCs could help central banks better manage economic cycles, especially when the constraints of the zero lower bound on interest rates are removed.

However, there are notable trade-offs to consider. Poorly calibrated CBDC designs could lead to excessive bank disintermediation, higher loan spreads, and increased liquidity risks during crises. The overall macroeconomic effects would depend heavily on design choices – such as remuneration rates, access policies, and holding limits – as well as the availability of tools to mitigate potential disruptions to banks and financial markets.

Challenges CBDCs Pose to Financial Stability

While Central Bank Digital Currencies (CBDCs) offer the promise of improved efficiency and more effective monetary policy, they also come with significant risks to financial stability. Policymakers must navigate these challenges carefully. According to the International Monetary Fund (IMF), there are at least six ways CBDCs could impact stability, with particular emphasis on bank funding, run risk, and cross-border flows. Below, we explore some of the most pressing concerns.

Bank Disintermediation and Profitability Risks

The ability for households and businesses to hold secure digital liabilities directly with central banks could lead to a significant shift away from traditional bank deposits. If CBDCs offer competitive interest rates and features similar to those of commercial bank accounts, the migration of deposits could happen rapidly.

For example, U.S. data based on economic models shows that when the policy rate is at 5%, banks can maintain a 2.5-point profit margin. However, with the introduction of a competitive CBDC, that margin could shrink to just 0.7 points, severely impacting bank profitability. The extent of this disintermediation depends on several factors, including how easily CBDCs can replace deposits, the attractiveness of their interest rates, and the availability of alternative funding options. Banks that rely heavily on retail deposits or have weaker capital reserves may face greater challenges, potentially leading to reduced lending or higher loan rates. This, in turn, could tighten credit availability across the broader economy.

Bank Run Risks and Liquidity Problems

CBDCs could also heighten the risk of bank runs, particularly during times of financial stress. Unlike traditional cash withdrawals, which require physical effort and time, moving funds from a bank account to a CBDC wallet can happen instantly. This lack of delay could accelerate deposit outflows, leaving banks and regulators with little time to respond. The result? Liquidity shortages and fire-sale dynamics as banks scramble to meet withdrawal demands.

The IMF highlights that this "run risk" is a unique challenge posed by CBDCs. When trust in banks erodes, deposits could quickly shift into CBDCs, which are seen as risk-free central bank liabilities. This rapid movement compresses the time available for intervention. According to the European Central Bank, banks might need to hold larger reserves to counter these risks, fundamentally altering how they manage liquidity.

Cross-Border Effects and Currency Internationalization

When CBDCs are used across borders, they introduce new complexities related to capital flow volatility and currency substitution. For instance, if people in one country can easily access and transact using a foreign CBDC – like a digital dollar issued by the Federal Reserve – it could undermine the monetary independence of smaller or less stable economies. In extreme cases, this could lead to digital "dollarization" or "euroization", making it harder for local central banks to manage financial conditions or act effectively as lenders of last resort.

Uncoordinated CBDC development could also worsen exchange rate pressures and complicate international monetary policy. Faster, cheaper cross-border capital flows could amplify these issues. The degree of impact would depend on factors such as how open a country’s capital account is, the credibility of its domestic policies, and the depth of its financial markets. For the United States, while a digital dollar might strengthen the currency’s global role, effective coordination with international partners would be critical to avoid unintended disruptions to global financial systems. These challenges highlight the importance of designing CBDCs with international collaboration in mind.

sbb-itb-8c45743

Design and Policy Solutions for CBDC Integration

Integrating Central Bank Digital Currencies (CBDCs) into the financial system comes with its challenges, but careful design and policy measures can address potential risks. Adjusting factors like interest rates, access levels, and holding limits can help mitigate these concerns. The International Monetary Fund highlights that by fine-tuning access, supply, and remuneration, central banks can minimize disruptions to monetary operations. Below, we dive into key design strategies to ensure CBDCs support financial stability.

Setting CBDC Interest Rates and Access Limits

One way to reduce the risk of disintermediation – where funds move away from traditional banks – is through tiered remuneration. U.S. data suggests a practical approach: offer a slightly lower interest rate on smaller CBDC balances while reducing or eliminating interest on larger holdings. For example, a U.S.-based model could set the rate at 1% below the policy rate for balances up to $5,000, drop it to 0% for higher amounts, and cap total holdings at $25,000.

This structure encourages using CBDCs primarily for payments rather than long-term savings, keeping traditional bank deposits more appealing for larger balances. The European Central Bank is also exploring safeguards like holding limits and "waterfall" features, which automatically convert funds between bank deposits and CBDCs to maintain bank funding and ensure smooth monetary policy transmission.

Protecting Banks and Credit Supply

To prevent funding challenges for banks, central banks must be ready to step in with reserves to replace lost deposits. Tools like standing lending facilities and discount window access can provide predictable, collateralized funding when retail deposits shift into CBDCs. Additionally, term funding schemes that tie central bank credit to actual loan origination can help sustain lending during the transition.

When banks and markets trust that reserves will be available to cover CBDC-related outflows, concerns about a funding squeeze are greatly reduced. Updating liquidity coverage rules and conducting stress tests that factor in CBDC adoption can further strengthen the system.

Preventing Bank Runs and Pro-Cyclical Flows

CBDCs allow for near-instantaneous money transfers, which could amplify risks during financial stress. To counter this, measures like daily or per-user conversion caps can limit rapid outflows from banks. These caps could be dynamically tightened in response to stress indicators, such as rising funding spreads or increased deposit withdrawals.

In times of heightened stress, temporary rate adjustments or small conversion fees can slow the pace of outflows. Cooling-off periods for large transfers can also help smooth transitions and protect bank liquidity.

Coordinated Cross-Border CBDC Frameworks

Introducing CBDCs on a global scale requires international cooperation to prevent issues like exchange rate volatility and currency substitution. Collaborative efforts, such as the Bank for International Settlements Innovation Hub’s mBridge and Project Dunbar, are exploring multi-CBDC platforms with shared technical standards and policies.

Effective coordination could include agreements on nonresident CBDC holding limits, shared frameworks for anti-money laundering and identity verification, and standardized messaging systems. For the U.S., working closely with partners like the European Central Bank can help ensure a U.S. digital currency strengthens the dollar’s global position without causing unintended disruptions to international financial systems. The ultimate aim is to achieve interoperability that enhances efficiency while maintaining financial stability and monetary independence.

What CBDCs Mean for Payment Providers and Businesses

CBDCs in Merchant Payment Flows

As central banks refine their CBDC frameworks to support monetary policy, merchants stand to gain from the efficiencies these digital currencies bring to payment processing. CBDCs introduce a direct settlement channel, allowing digital dollars to move through central bank money. This could simplify the payment chain by bypassing multiple card networks and processors. Instead, a CBDC payment might flow directly from a customer’s CBDC wallet, through a payment service provider, to a merchant’s settlement account or CBDC wallet. For U.S. e-commerce businesses, this could mean CBDC payments appear as an option alongside cards and ACH during checkout, offering real-time finality similar to instant bank transfers but backed by central bank settlement.

At the point of sale, CBDCs enable direct, real-time settlement through methods like QR codes or wallet taps, cutting out the typical 1–2 day delays. While transaction aggregation and reconciliation services would still be needed, businesses – especially small ones – could benefit from improved cash flow since funds would be accessible immediately after a transaction.

When it comes to cross-border transactions, CBDCs could bring even greater advantages. Currently, these payments rely on correspondent banking chains, which involve multiple foreign exchange spreads, compliance checks, and delays of 1–3 business days. Multi-currency CBDCs could allow direct central-bank-to-central-bank settlement, reducing intermediaries and enabling near real-time transfers across borders. For U.S. e-commerce merchants serving international customers, this could mean faster access to funds, more transparent foreign exchange rates at checkout, and lower transaction costs compared to traditional wire transfers or card-based cross-border payments. However, successfully integrating CBDCs into existing systems will require expertise to bridge the gap between traditional and CBDC infrastructures.

How Payment Partners Like Secured Payments Can Help

Even with streamlined settlement rails, businesses face the challenge of integrating CBDCs into their operations – a task that specialized payment partners can simplify. Secured Payments can serve as a single integration layer, connecting merchants’ existing gateways, POS systems, and ERP software to new CBDC networks. This ensures businesses can accept CBDC payments without overhauling their current payment systems or disrupting daily operations.

Payment partners can design and implement CBDC-ready checkout and point-of-sale solutions, optimize routing logic to balance cost and risk across payment methods, and provide unified reporting that consolidates CBDC transactions with traditional payments. For industries prone to high chargebacks or fraud, providers like Secured Payments can assess how CBDC settlement – offering lower chargeback risks but more permanence in fraudulent transactions – impacts risk profiles and pricing strategies, then adjust merchant account structures accordingly.

Beyond technical integration, payment partners offer consulting services to help businesses prepare for CBDC adoption. This includes updating cash management policies to handle CBDC balances, enhancing AML/KYC and transaction monitoring processes to meet stricter reporting requirements, and training finance teams on managing CBDC balances versus traditional bank deposits. By partnering with experienced providers, businesses can participate in early CBDC pilots and scale adoption smoothly as CBDC infrastructure becomes widely available.

Conclusion: The Future of CBDCs and Monetary Policy

Central Bank Digital Currencies (CBDCs) are shaping up to complement, not replace, the traditional tools of monetary policy. Institutions like the Federal Reserve and other central banks will continue their roles in adjusting interest rates and managing money supply. However, they may increasingly rely on digital instruments – potentially even interest-bearing ones – that connect directly with households and businesses.

The success of CBDCs hinges on thoughtful design. Tools such as tiered interest rates, limits on holdings, and access restrictions need to be carefully balanced. These mechanisms can strengthen how monetary policy impacts the economy without causing large-scale withdrawals from traditional banks. For example, an interest-bearing CBDC could enhance how policy rate changes affect deposits and loans, but only if safeguards are in place to prevent excessive disruption to banks. In the U.S., the Federal Reserve has stressed the importance of preserving the central role of commercial and community banks, especially in providing credit to small businesses and households. This approach envisions a future where traditional banking and digital currencies work together seamlessly.

Rather than fostering competition, the future likely points to coexistence. Banks will remain the primary providers of credit and financial services, while CBDCs could act as the safest digital asset issued by central banks. Payment providers such as Secured Payments are well-positioned to play a critical role, enabling businesses to integrate CBDC payments alongside existing options like cards and ACH. By managing the complexities of real-time settlement in central bank money, these providers can help streamline payment systems. This setup reflects earlier discussions on simplifying merchant payment processes. A public–private partnership model like this can drive innovation in the private sector while maintaining the Federal Reserve’s pivotal role in anchoring the monetary base.

To make this coexistence model work, phased pilot programs, strong collaboration across agencies, transparent governance, and adherence to international standards will be crucial. These steps can help manage adoption, provide liquidity tools during periods of rapid uptake, and ensure monetary policy remains effective as digital currencies reshape global payments. With robust regulation and clear communication, a well-designed CBDC has the potential to modernize how money functions while maintaining financial stability and public confidence. Altogether, these efforts underline the importance of balancing new digital tools with the need for a stable financial system.

FAQs

How could CBDCs change the role of traditional banks?

Central Bank Digital Currencies (CBDCs) could reshape the traditional banking system in profound ways. By allowing individuals to transact directly with the central bank, CBDCs might reduce the need for commercial banks to serve as intermediaries for payments and deposits. This change could disrupt how banks generate money through lending, potentially impacting their profitability and their role within the financial system.

On top of that, CBDCs could lead to a more centralized approach to monetary control. Central banks would gain new tools to directly manage the money supply and fine-tune monetary policy. While this opens doors for new opportunities, it also presents challenges for traditional banks as they navigate this evolving digital financial environment.

How can bank runs be prevented with CBDCs?

To safeguard against bank runs in a system featuring central bank digital currencies (CBDCs), several strategies can be employed. One approach is implementing withdrawal limits to regulate the movement of funds and prevent sudden, large outflows. Another key measure is ensuring sufficient liquidity buffers to address spikes in demand effectively. Designing tiered account structures can also help by distinguishing between retail users and institutional participants, tailoring rules and limits accordingly. Finally, robust central bank support plays a crucial role in reinforcing public confidence and preserving trust in the financial system.

How could CBDCs impact global monetary policy?

Central Bank Digital Currencies (CBDCs) could transform how global monetary policies function, especially by simplifying cross-border transactions. By minimizing reliance on traditional currencies and cutting out financial intermediaries, CBDCs have the potential to make international payments quicker, more straightforward, and possibly less expensive.

This change might lead to greater currency stability, but it could also bring new challenges, depending on how these digital currencies are rolled out. On one hand, CBDCs could open doors for better global monetary collaboration; on the other, they might fuel heightened competition among currencies on the world stage.