The Payments Industry is a fast-paced environment that is continually evolving owing to new payment systems, mergers and acquisitions, and technological advancements. We see payment processing firms play a more prominent position in the payments market.

Particularly as technology advances, many of them partner with conventional financial institutions to appeal to the new consumer and retailer preferences. In the past, payment processing was merely about managing the flow of money.

However, today’s payment processors redefine the consumer experience and allow business owners to handle their companies with unprecedented ease.

Channels and Means Have Evolved

Money and the concept of exchanging it by transfers have come a long way from their conception. Money has taken several types, sizes, and kinds, ranging from commodities to grain, metal coins to paper, bank accounts, and e-wallets.

Payments have progressed from barter (exchanging commodities for grains) to token (exchanging coins and cash on paper) and cash pooling (bank balances and deposits) and cashless payments (credit cards, checks, e-wallets).

Payments are changing at a breakneck pace, with different services, networks, and payment tools appearing regularly. If customer behavior changes, Omni commerce – the option to pay using the same approach whether in-store, online or on a mobile device – becomes more anticipated. As a result of this transition, retailers would need to adapt to quick, convenient, and stable mobile payments.

In 2017, the payments market underwent a transition. The ongoing fight with alternate payment platforms will escalate, forcing incumbents to take drastic action in emerging markets. The following are some primary drivers:

1. Real-Time Payments (RTP)

RTP reflects a new stage in developing the payments sector, with many core features that set it apart from existing payment methods, including speed, value-added communications capability, and instant transaction status availability. RTP would offer financial institutions the tools they need to innovate to satisfy consumer demand.

2. Distributed Ledger Technology (DLT)/Blockchain

Among its many uses, Blockchain can radically transform the financial transaction management cost model. Both computing may also be performed through a distributed device network or in the cloud, without the need for expensive data centers or mainframes.

3. Payments Expansion of Non-Physical Interfaces

External partners (Amazon, Google, Facebook, and Apple) are challenging traditional interfaces in two ways: voice assistants and virtual reality. With the addition of NLP and image recognition, connected assistants have become more innovative and more practical.

As voice-first solutions advance, relying on physical interfaces, especially mobile, may no longer guarantee long-term relevance. Classic interfaces and solutions designed for them would eventually fall out of favor when Facebook becomes concerned with destroying the mobile to own virtual space.

4. Unified Platforms

UPI is an open-source interface for the modern era that allows for quick convergence with different payment systems. A single payment API and a range of supporting APIs power UPI. UPI presents a whole different ecosystem for the financial services sector.

UPI was the beginning of a “journey to a single payments network.” UPI is a benchmark for where the payments environment could be heading with the oversaturated payments world, where so many “pays” won’t let anybody win.

Customers are confused by disparate interactions around companies, which, combined with a small client base, limits opportunities for all payment service providers, old and modern. The payments market needs to move away from many aging and costly networks and schemes and toward a centralized network that can handle all payments.

Customers would provide a shared payment experience (based on seamless device interoperability, similar to mobile telephony) in the future, rather than a single payment network.

Standard Terms Related to Payments

The conditions of payment may be perplexing, and acronyms abound. What is the authorization rate? PCI, POS, and PSD2? A dozen of the more popular words and phrases, along with their meanings, are mentioned below.

Acquiring bank (or acquirer):

A financial entity or bank that allows a business to receive payments. This is, in other words, the company’s bank.

Authorization

When a cardholder, such as a bank or credit card provider, verifies a shopper’s order to buy anything, it is called authorization. When a cardholder’s application is accepted, the issuer places a lock on the permitted balance on the cardholder’s account. This is to brace for the capture (actual funds transfer). The number of transactions that are approved is known as the authorization rate.

Card Schemes

Visa, Mastercard, American Express, Discover, and UnionPay are the leading card networks, but a payment network is not the same as a credit card firm. Card networks set the technological infrastructure and guidelines for payment transactions, and they charge for the service.

Chargeback

When a shopper does not comply with a fee on his or her bill, the first option is to request a refund. If the dealer declines, the shopper will file a chargeback with her bank.

Based on facts provided by the sides, this is the beginning of a dispute procedure to determine who is responsible for the transaction. Fraud, faulty products, or merchandise not shipped are also possible reasons for a chargeback.

Fraudulent Activity (fraudulent payment)

This indicates that a rogue entity attempted or executed a trade.

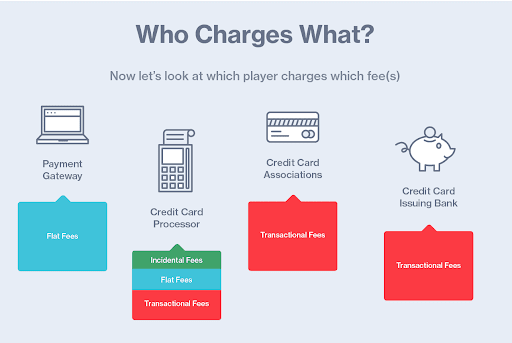

Interchange Fee

The dealer pays a charge to the receiving bank and the shopper’s issuing bank for each card-based purchase. You can determine the fees by the form of the card used, the amount of the charge, and the retailer group.

The Issuer (or Issuing Bank)

Consumers are sent a variety of cards, including debit and credit cards, by the issuing bank. To put it another way, the issuing bank serves as a shopper’s bank.

Local Payment Options (or alternative payment methods)

Any payment system that is not associated with an extensive credit card network. In specific markets, card purchases are not the preferred mode of payment. Bank deposits, direct debit, digital wallets like Apple Pay or Samsung Pay, or cash-based systems are used in some instances.

Point of Sale (POS)

A point of sale solution is a hardware and software mix that allows a shopper to buy products and services in a physical store. When it comes to providing secure contactless payment solutions, the point of sale is an integral part of the payments ecosystem.

Payment Gateway

A service that enables merchants to accept payments through e-commerce, in-app, and point-of-sale for a wide range of payment methods. The gateway is usually a database server to which a merchant’s website or POS scheme is connected.

It is not specifically active in the money flow. A payment gateway is a mechanism that links several purchasing banks and payment methods into one.

Payment Service Provider (PSP)

An organization that will link to several acquiring and payment networks and integrates the features of both payment gateways and payment processors.

PCI Compliance

The major card networks developed the PCI DSS (Payment Card Industry Data Security Standard) to improve cardholder data security and reduce the possibility of fraud. PCI compliance is required by all businesses that process credit cards.

Final Words

When companies and customers move money from cash and checks to digital payment systems, the power dynamics in the payments market are shifting. Cards dominate In-store shopping, but mobile wallets like Apple Pay are rapidly gaining traction.

Around the same time, as smartphones draw a growing share of digital shopping, e-commerce would eat into brick-and-mortar retail. When they become more attractive and valuable than ever, digital peer-to-peer (P2P) applications displace cash in consumers’ daily lives through generations.